Table of Contents

ToggleIntroduction

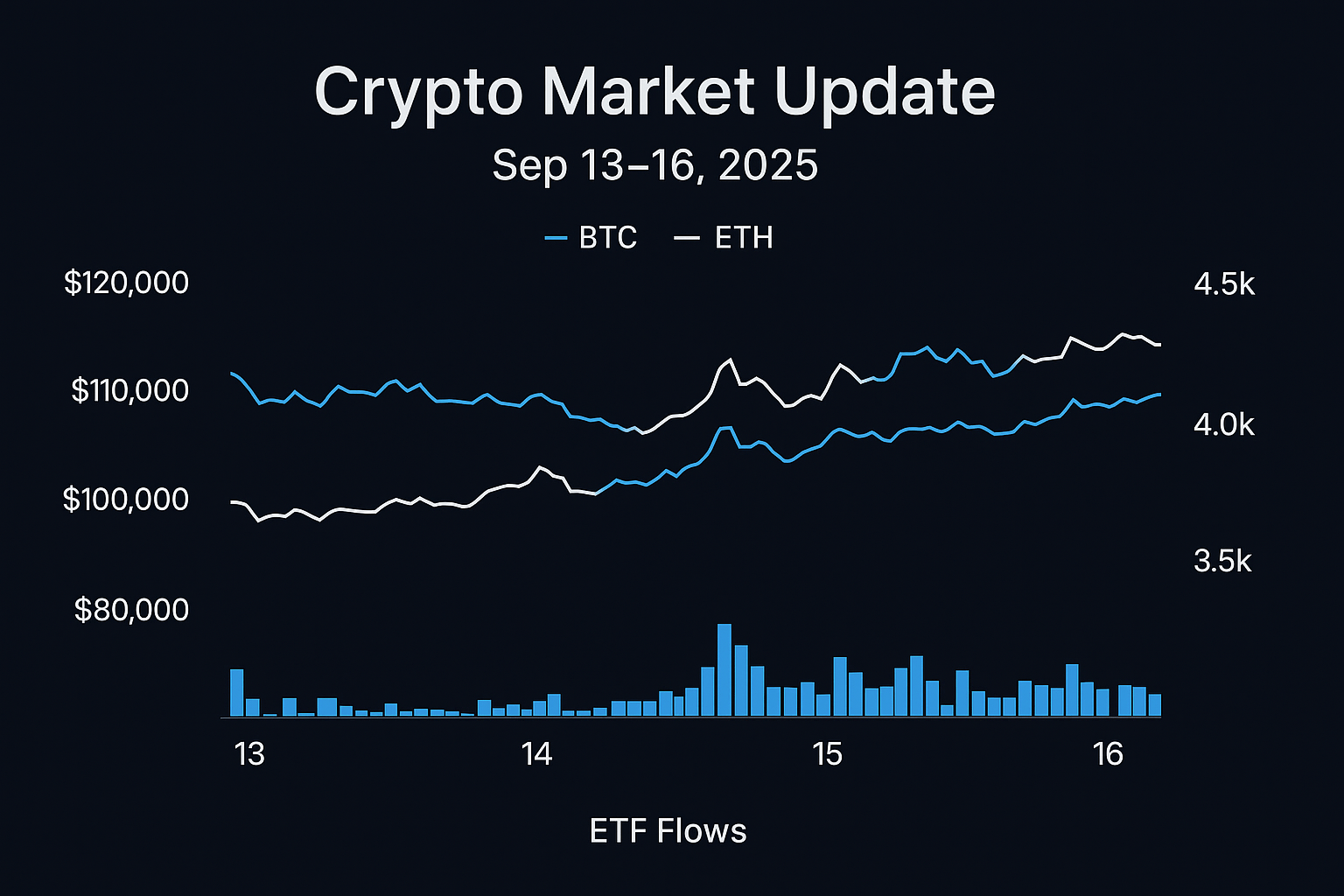

The cryptocurrency market entered a period of consolidation from September 13 to 16, 2025, following the high-energy performances in the market at the beginning of the month. Bitcoin (BTC) stagnated at the level of about $115,000, and Ethereum (ETH) stood at the middle of the 4,000. Trading volumes and volatility slowed down instead of explosive moves, signifying a market that is in the wait-and-see mode.

What was so significant about this window was not necessarily the sideways trading but the structural flows and macro background that were influencing sentiment. On the one hand, there were steady inflows of spot Bitcoin ETFs and new Ethereum investment products, and this indicated that regulatory vehicles were being used by institutional allocators to deploy capital in crypto again. On the flip side, speculations of an imminent Federal Reserve interest rate reduction boosted investor confidence in risk assets and offered an enabling atmosphere to crypto consolidation.

Some of the altcoins, such as Solana (SOL) and XRP, had a better performance. Some fresh Ethereum forecasts were also issued by analysts, including a $4,300 end-of-year base case by Citi, which was met with controversy. Meanwhile, the traders pointed to the contribution of on-chain exchange outflows, ETF-based demand, and neutral funding rates to the establishment of near-term market stability.

The lesson that has been learned during these three to four days is that the market is at a crossroads. The ETF flows are offering a structural bid, and the macro policy expectations are offering the risk appetite tone. These forces in action will presumably decide whether BTC and ETH go further into new cycle highs- or a correction takes place should inflows crack or Fed policy prove to be even more disappointing.

This Article discusses the price movement, institutional activity, macro factors, analyst opinion, altcoin news, and scenario review of September 13-16, and provides a systematic examination of why the phase could be critical to the next phase of the crypto cycle.

Price Action and Immediate Market Picture

Between September 13 and 16, 2025, the crypto market recorded controlled consolidation as opposed to the dramatic ups and downs that have dominated most of this cycle. Bitcoin (BTC) was fairly in the tight band around $115,000, indicating a pause just below the cycle high that it hit earlier in September. Ether (ETH) followed suit as it stayed at the mid-4,000s range following an impressive upward trend in the past weeks.

There was an even market as evidenced by the trading activity. Volumes were neither panic selling nor euphoric buying. Similarly, volatility subsided against the extreme volatility of late summer. This composure mirrored a more general mood: traders as well as institutions were awaiting more clearly defined macro indications before they would appreciate fresh capital in volume. The next steps of the Federal Reserve policy were looming large, and most preferred to ensure that they were positioned at the middle level instead of going too far.

Both Bitcoin and Ethereum are technically building symmetrical triangles and consolidation patterns, which most analysts would see as a setup that may result in a breakout. A consolidation period following a strong run-up can be good, enabling the market to digest profits, blow out the weak hands, and reset the leverage. This creates a greater basis for the subsequent directional movement. Notably, the convergence was occurring in favourable ETF flows that gave credence to the bullish bias.

The price movement was perceived as cautiously positive by the market participants. BTC and ETH were able to sustain a high level, instead of the pullbacks that frequently succeed euphoric surges. Such resilience implied that buyers were ready to protect existing levels, especially when inflows into regulated investment products were not reduced.

Briefly, the short-term market conditions were those of pre-storm calm. The convergence indicated structural aids in institutional flows as well as macro indecision before Fed decisions. Traders considered this balance as a position that will soon either be resolved into a huge breakout or break as the trading catalysts come in the coming weeks.

ETF Flows and Institutional Rotation

Institutional inflows into regulated crypto products represented the defining characteristic of the September 1316, 2025, window and not wild price action. Following the summer of ambivalent flows, the attention returned squarely to spot Bitcoin ETFs and Ethereum exchange-traded vehicles, which jointly attracted consistent investments by professional investors.

In the case of Bitcoin, the narrative was simple: spot ETFs registered a series of several days of net inflows. Flow trackers have shown a specific high inflow on September 12, when close to $553 million was deposited into Bitcoin ETFs within one trading session. The same theme was solidified in the following days, and net positive flows persisted until September 15. This is important since ETF flows are institutional grade demands, capital lying in through demand that is of a custodial compliant, regulated investments, not speculative retail.

Ethereum followed suit. The ETFs are ETFs based on ETH, and significant inflows over the same timeframe were made, which is a significant milestone in the shift of Ether as a high-beta altcoin to an institutionally owned programmable asset. In addition to price exposure, staking yield dynamics provide ETF buyers with a twofold appeal as a speculative gain combined with a sort of yield-generation, which makes ETH positions increasingly competitive to conventional risk assets.

These ETF flows are not just numbers daily. They are a structural change in the microstructure of the market. The marginal buyer of crypto is changing as the institutional vehicles increase. Crypto is no longer dependent on the enthusiasm of retailers in the short term, but rather absorbing the stable demand of pensions, asset managers, and family offices that are coming in through ETFs. This can stabilize volatility, enhance liquidity, and transform the way supply-demand equilibrium shapes up on exchanges in the long term.

In other words, ETFs are the new face of crypto demand soon. They offered the structural bid that saw Bitcoin cementing above $115k and Ethereum holding the $4k handle as the global market awaited direction from the macro policymakers. The absence of this institutional rotation would have made the September calm look less strong.

Macro Backdrop – Federal Reserve and Risk Appetite

Previously, in case ETF inflows were the structural factor to support the resilience of crypto, the macro backdrop offered the psychological framework. It was in this period that the market players became more confident that the Federal Reserve was about to reduce the interest rates by 25 basis points. Such a forecast was the big shift in mood, especially when it came almost two years after a period of tight monetary policy aimed at controlling inflation.

So, what is the significance of this in crypto? First, the reduction of rates will reduce the yield on government bonds and other safe assets. It makes non-yielding or alternative yield-bearing assets more attractive, including Bitcoin or staked Ethereum. When investors are looking to get returns in a less lucrative world, they are likely to shift to risk assets, and crypto is likely to benefit as a result. Second, the indicator is a sign of a more accommodative liquidity environment that has been associated with better performance in equities, tech, and digital assets.

Market observers actively associated this rate-cut story with the ETF flows that were being recorded in Bitcoin and Ethereum funds. The integration of macro easing and structural adoption could have been a very attractive entry point to institutions, especially as crypto settled at higher levels. The moderate inflows even took on an added weight when they were viewed through the prism of rising risk appetite.

But the hope was not without a qualification. The markets were very sensitive to Fed messages as the rate-cut story was as much in support as possible. A surprise of a more hawkish nature (a delay in the cuts, or a smaller easing path, or fears that inflation persists) will reverse sentiments in a hurry. Crypto, like risk assets, is susceptible to swift repricing in case the expectations and the realities of the central bank are at variance.

Overall, the macro backdrop preconditioned the optimism of crypto in its guarded manner. The Fed initiative was not, as it was predicted, based on near-term fundamentals, but rather based on strengthening the belief that the liquidity tide can soon reverse in Favor of the risk-on assets.

Analyst Views and Forecasts

Combined with ETF flows and macro speculation, the September 13-16 period saw new commentary on Ethereum and crypto valuations on the part of analysts. These perspectives were both reassuring and controversial, and they show how institutional research still informs the expectations of the market.

The most significant release was done by Citi as it published a year-end Ether forecast on September 16. Citi analysts had forecasted a base case of 4,300 ETH by the end of 2025. This number was considerable since it was placed below the numerous optimistic scenarios in the market. Citi highlighted staking demand, institutional adoption, and network activity as the key value drivers of ETH but was more subdued in its tone than competitors. To other traders, the conservative prediction was a wake-up call that the increase in ETH is not necessarily going to increase at a linear pace.

Other banks and other research firms were more optimistic. Some alternative models had indicated the bullish projections of up to $7,500 on ETH in case of ongoing inflows of ETF, high staking returns, and rising adoption of Ethereum-based applications. These conflicting predictions reflected the high variation in the analyst expectations, as they had different assumptions on how users would behave, generate fees, and other market liquidity trends around the world.

The difference in analyst opinions was important in terms of sentiment. On the one hand, the markets were induced with caution by conservative estimates of respected institutions such as Citi, making the market unwilling to indulge itself. Conversely, optimistic forecasts were useful to maintain hope and support the story that ETH is one of the significant institutional assets in addition to Bitcoin.

The lesson learned by investors and traders was that the analyst forecasts are not guarantees but conditional. They are constructed based on assumptions, which may change quickly due to the macro policy, ETF demand, or on-chain adoption. These views were found useful in the market as scenarios, but they were not predictions that were binding.

Altcoins and Token Highlights

Bitcoin and Ethereum took up much of the institutional attention over the period of September 1316, but the altcoins were selectively strong, which serves as a reminder to the market that there are still pockets of performance that lie beyond the top two assets. Solana (SOL) and XRP were some of the best-performing off their own narratives and investor flows.

Solana remained the subject of attention due to the activity of the developer, growth of the ecosystem, and its status as a high-performance blockchain. Over the past few months, there has been a trend toward Solana-based projects in decentralized finance (DeFi), non-fungible tokens (NFTs), and infrastructure tooling. That action carried over into periodic rallies of SOL, even whilst in these phases of consolidation. Analysts also noted that the fact that Solana has continued to grow its user base and continues to attract developers is what makes the token more than a mere speculative asset, but rather a viable Ethereum alternative in some application areas.

XRP also proved comparatively strong, as it has been associated with international payments since the time immemorial and has been supported by hopeful speculations of regulatory certainty. Following several years of uncertainty, which was associated with U.S. litigation, the XRP story has changed to a more stable and payment rail acceptance. This stance made it a popular one with traders interested in exposure outside of BTC and ETH, particularly during periods of regulatory or macro-driven excitement.

In addition to these two, there was commentary interest in infrastructure-tied tokens, staking, and more recent narrative-driven sectors. Although these assets were still a tiny fraction in terms of market capitalization, targeted rallies pointed to investor interest in thematic trades, be it in metaverse projects, DeFi innovation, or blockchain scaling solutions.

That notwithstanding, this week had a structural narrative: institutional flows were too many into Bitcoin and Ethereum ETFs. The rallies of altcoins, despite being significant, were still subordinate to the overarching trend of capital being regulated and flowing into the majors. Nonetheless, their comparative power remained a helpful indication that crypto cycles tend to uplift different ecosystems, and agile investors are still ready to find opportunities on top of BTC and ETH.

On-Chain and Derivatives Signals

In addition to prices and flows of ETFs, the period of September 13-16 provided valuable indications on on-chain activity and derivatives markets. These signs offered a better understanding of the direction of the capital flow under the water, and whether the traders were going to be aggressive speculators or prudent accumulators.

The exchange outflows of Bitcoin were one of the trends. Statistics depicted that BTC has consistently exited the exchange wallets, a trend that is frequently associated with savings by long-term holdings or ETF-related custody options. On withdrawing coins from exchanges and putting them into cold storage or a custodial account, the supply of liquid decreases. In the past, this has been associated with more price floors during the period of consolidation. These outflows played a strengthening role in the perception that institutions were assisting to absorb supply in the context of the increasing ETF inflows.

In the derivatives, the open interest (OI) and the funding rates provided a moderate picture. OI on the largest futures exchanges moved marginally upward, indicating that traders were returning to the markets after a low-key few weeks. Funding rates, however, stayed at the neighbourhood of neutral or a little positive, that is, there were neither bulls nor bears that dictated the leverage application. It was a refreshing change compared to the previous period of the year, where the extreme long or short positioning resulted in forced liquidations and increased volatility.

Flow channels were another structural signal. An increasing portion of fresh buys in USD was channelled through ETFs as opposed to retail exchange deposits. This development highlights the change in the entry points of capital in crypto. The market is also taking up institutional demand that is controlled and predictable, as opposed to relying on the primary dependence of speculative retail inflows.

A combination of these cues created an image of controlled involvement. Supply was secretly narrowing through custody-related outflows, leverage was contained, and ETFs were becoming the primary source of capital. This mixture decreased the probability of liquidation cascades in the near term but left the market at the point of a decisive action once macro or flow catalysts are met.

Market Psychology and Technical Narratives

The market psychology during this consolidation period was characterized by inhibited optimism. Both traders and investors acknowledged that Bitcoin and Ethereum were already enjoying great returns earlier in the cycle, and the stalling at 115,000 and 4,000s, respectively, was being viewed as a refreshing break and not an indicator of fatigue.

Technically, analysts identified symmetrical triangle patterns and range-bound constructs over significant periods of time. Such arrangements are usually indications of a market ready to break out. The debate was on the direction: would prices rise on the inflows of ETF, dovish Fed expectations, or would a policy surprise or a decelerating rise in flows cause a fall?

Sentiment measures indicated that the retail involvement had calmed down against the euphoria touches seen in the first half of the year. This was not necessarily bearish per se, but less retail fever usually enables markets to gain firmer foundations as weak hands are shaken out. In the meantime, the institutional desks, which are led by ETF allocations, were perceived to offer a stable underlying bid. The equilibrium in the market formed a market psychology that was characterized as calm yet alert.

The traders were positioning their strategies based on catalysts of events. It was observed that the next directional move of importance will probably depend on Federal Reserve communications or ETF flow headlines. But without those stimuli, the way of least resistance was horizontal. Nevertheless, the strength of BTC and ETH close to high levels was an indicator that bulls still had an edge.

Finally, the psychology of September 1316 was less momentum chasing and positioning for the breakout. Investors were ready to support areas, technical indicators indicated compression, and ETF inflows served as a psychological floor, which increased confidence. The atmosphere of the market, briefly, was tolerantly bullish.

Key Risks Over the Next 1–4 Weeks

Despite a market tone between Sept 13 and 16, 2025, of a cautious bullish, some near-term risks would easily overturn the script. The most important one is Federal Reserve messaging. The 25-basis-point reduction has been priced in by markets, and any indicator by the Fed of a delay in cuts, or a reduction smaller than anticipated or conditional on stubborn inflation, would probably cause swift de-risking of rate-sensitive assets, including crypto. Fed commentary may be high impact since it alters the liquidity environment on which ETF demand and risk appetite in general are based.

A second significant risk is an inflow reversal or stagnation in ETFs. It has been reported that the inflow streak into spot Bitcoin ETFs (an impressive single-day intake of approximately $552553m was reported on September 12) has been a structural prop to BTC and thereby risk-on positioning in crypto as well. When these flows are decelerating or receding, or when a market is absorbing a big redemption, the marginal buyer will dry up, and the price action may unwind abruptly, especially since on-exchange liquidity has been weakening, as coins move into custody.

There is always a tail risk of regulatory and enforcement shocks. Announcements by major jurisdictions (U.S., EU, India, China) may create disproportionate volatility, including new restrictions, aggressive enforcement actions, or unfavourable court decisions. Past events reveal that headlines that are driven by regulation can unravel leveraging and create cascade selling.

Another issue is that of derivatives market stress. During the Sept window, funding rates and open interest were measured, but a quick pick up in leveraged longs (or excessive short squeeze) would be able to move and cause forced liquidations. Early warning indicators of traders should be funding rates and OI.

Lastly, flash drops can happen due to idiosyncratic on-chain events (massive smart-contract exploits, large whale withdrawals to exchanges, exchange custody, etc.), which do not depend on macro or ETF dynamics. Cumulating these risks suggests position sizing discipline and active follow-up: a benign macro/flow environment would justify the benign bullish position, but any of the risks would substantially enhance the downside volatility.

What the Flows + Macro Combo Means for Different Participants

The interplay between institutional ETF flows and the changing macro policy perspective is of very different implications for a type of market participant. Long-term allocators to short-term traders, institutional desks, and so on, interpret the same signals in their own ways.

The consistent inflows into spot Bitcoin and Ethereum ETFs are a structural positive to long-term holders and allocators. The products offer institutional-friendly vehicles that satisfy all the requirements of orchestrating compliance with the institutional exposure to crypto. A clear route is now available to pension funds, endowments, and family offices who may have been reluctant in the past because of custody, compliance, or liquidity concerns. To them, the rising use of ETFs and a likely period of relaxation by the Federal Reserve creates a ground on which to allocate strategically. They are not interested in volatility daily, but in crypto becoming an acceptable asset class.

The tale is different for active traders. The ETF flows give a floor to the bid that minimizes downside tail risk, although the macro events like the Fed announcements are the most important short-term catalysts. Traders know that any changes in expectations of the rates can cause the crypto sentiment to swing dramatically. Their trading regime is based on range trading in times of consolidation and pivotal aggression when there are catalysts in place. ETF flow indicators and derivatives tracking, such as funding rates and open interest, will be useful in measuring short-term positioning.

To the institutional desks and asset managers, ETFs are not a product but an entry point to scale exposure. Regulated wrappers are favoured by compliance teams and regulators, and that is why asset managers can fulfil the demand of the clients in the most efficient way with ETFs. In this regard, the ETF development is simply a measure of both adoption as well as a structural transition of ownership: more crypto exposure will be increasingly contained within regulated goods, altering liquidity patterns and volatility over time.

Notable Headlines That Shaped Sentiment

There were a few impactful headlines between the 13th and 16th of September 2025 that influenced the market interpretation of investors and traders. These narratives did not simply inform; they acted decisively on the placement, feeling, and, in certain instances, capital flows.

The strongest and the initial story was that of ETF inflows. On September 12, single-day net inflows into spot Bitcoin ETFs hit as high as 553 million and were reported in mainstream financial media. This was not a mere piece of data but was viewed as evidence that institutional allocators were returning to crypto on a large scale. Sequential days of net positive incoming flows into both Bitcoin and Ethereum ETFs were followed up with those words, thus strengthening the perception that regulated investment vehicles were turning into a fundamental support of demand. These headings contributed to the belief that the condensation of BTC at $115k and ETH at $4k+ was supported by material structural flows.

The second sentiment driver was through the analyst community. On September 16, Citi published its end-of-year Ethereum projections, with a conservative base case of $4,300. This was remarkable since it was not aggressive compared to certain bullish projections that were floating in the market, and the other banks were releasing ETH targets that were nearer to 7,500 dollars. The Citi note coverage created discussion concerning the short-term driver of ETH valuation, specifically staking yields, institutional adoption, and network activity. The forecast itself was not a dramatic one, but the disparity in the opinions of analysts created a story of uncertainty and dispersion, which was interpreted by the traders through a more cautious positioning.

Lastly, there was a psychological tailwind that came with macro-related headlines. Press reports emphasized emerging market expectations of an imminent Fed rate reduction, with options of a 25-basis-point cut in the rate movement already priced in, which supported the ETF-based optimism.

Combined, these headlines, including ETF inflows, the ETF forecast of Citi, and Fed cut expectations, were the foundation of market sentiment. They touched on three different levers: flows, valuation, and macro policy. To traders, they had become the fundamental compass by which they could set strategy over a week, which was more of a narrative than pure volatility.

Data Snapshots – Selected Numbers

To comprehensively interpret the market window of September 13 16, it is only logical to base the discussion on the hard data. The factual basis for the narratives that informed sentiment was many price trackers, flow monitors, and analyst reports.

Beginning with the majors, Bitcoin (BTC) was consolidating between $115,000. This was the second consecutive level lower than the high in the cycle in early September, which highlights the fact that, despite the deceleration in momentum, BTC was trading at historical highs. Ethereum (ETH), meanwhile, held steady at the middle of the $4,000s- many trackers gave the average between 4,400- 4,600 between September 1516. Both assets were able to keep their levels high even as the volume was softer, which was a sign of support by the inflows of ETFs and macro-optimism.

This was supported by the flow data. On September 12, spot Bitcoin ETFs recorded an impressive net inflow of around 553 million, one of the largest single-day allocations made to date. Follow-up sessions continued to record good net buying up to September 15, a run that boosted trust in the institutional demand. Consecutive inflows were also experienced in Ethereum ETFs but with lesser magnitudes, indicating that ETH was gaining momentum among allocators as a programmable yield-bearing instrument.

Exchange outflows of BTC were seen on-chain, which is also in line with ETF-led accumulation of custody. These liquidity leakages affect the liquidity supply, which was regarded as being bullish to medium-term price support. Meanwhile, the derivatives markets were portraying a picture of moderation: open interest was moving in the right direction, although funding rates remained firmly within the neutral area, which indicated the presence of speculative leverage, though not excessive.

There was one more piece of data: the ETH base case of Citi at the end of the year, which was 4,300 and had both bullish and bearish variants. The forecast, although not universal, was a major benchmark to investors who evaluated the path of ETH in the framework of institutional demand and staking economics.

A combination of these snapshots painted a straight line: the prices were falling into line, the inflows were accumulating, the supply was shrinking, and analysts were divided. The combination predetermined the breakout or the correction, which occurred on the condition of how the future macro catalysts would develop.

Scenario Framing – Bullish, Neutral, Bearish Paths

The uncertainty in the markets has made traders as well as investors relocate toward scenario analysis, where they frame the possible results rather than relying on one forecast. This was not an exception to the period of September 13 -16, 2025. As the inflows into ETFs persisted and the macro policy outlook changed, there were three likely short-term scenarios: bullish breakout, neutral consolidation, and bearish reversal.

The bullish baseline is where ETF inflows are flat and the Federal Reserve cuts the rate by 25 basis points, as the markets anticipate universally. This confluence supports institutional demand and relaxes financial conditions, and promotes risk-on positioning. In the given case, it is very possible that Bitcoin would burst out not only of the current consolidation range of above 115k, but also to even new cycle tops. With both ETF inflows and staking stories backing it up, Ethereum may also rally significantly higher, and some analysts are looking at points in the 5,500-6,000 range. This would be beneficial to the altcoins since the capital would move out of majors when confidence is gained.

The neutral scenario presupposes that the inflows to ETFs will be maintained at a decreased rate, whereas the Fed signals are dovish but no longer foolhardy about inflation. In this scenario, BTC and ETH would be prone to range-trading, as Bitcoin would be trading between $110k and $118k, and Ethereum would be ranging within $4,200 and $4,700. Technical, news-based volatility spikes would be leaned on by the traders, but the momentum would be held by a lack of a definitive macro or flow push.

Assuming hawkish surprise by the Fed (either postponing the cuts or threatening sustained inflation) or unexpected changes in ETF flows, the bearish scenario occurs. In case inflows are inverted to outflows, the structural bid in the market is compromised, and BTC may fall quickly, with one support level around 100k-105k. Ether may fall up to $3,800 to $4,000, and altcoins would tend to lag since they do not have sufficient liquidity. Derivatives markets may intensify the movement through forced liquidation, whose volatility is forced to increase.

Finally, such scenarios demonstrated the conditionality of the next move of crypto. Although the underlying skew was to the bull’s courtesy of institutional inflow and declining expectations, one macro shock could get the market quickly re-pricing.

Practical Takeaways & Watch List (What to Monitor Next)

To the investors and traders trading in the crypto market between September 1316, 2025, the interaction of ETF flows and the Federal Reserve policy proved to be the force. To position successfully in the next several weeks, the participants should pay attention to a clear set of signals that condition short-term momentum and the long-term structure.

The best options are at the top of the list, with daily ETF flow trackers provided by such sources as The Block, Farside, and BitBo. These are the most representative data on the demand in institutions. Constant inflows validate the structural support of Bitcoin and Ethereum, and an abrupt deceleration, or even the reverse, to net outflows, would dissolve that cushion and subject the prices to greater corrections. The ETF flows, in a nutshell, have become the heartbeat of the market.

In addition to flows, Fed communications and U.S. macroeconomic prints (CPI, PPI, and job reports) are essential. The expectations of the central bank to cut the rates are already priced in the asset markets, thus any hawkish surprise would shake risk assets, including crypto. Even minor alterations in the tone need to be monitored by traders not only through FOMC statements but also through Fed speakers because such alterations might affect the global liquidity situation.

On-chain data is also essential. Outflows of BTC and ETH indicate institutional custody demand should absorb supply, which is a positive structural picture. On the other hand, huge inflows of transfers or exchange of whales can be an indication of possible selling pressure. Close attention should also be paid to the derivatives position, as indicated in open interest rates and funding rates, and where there are unexpected spikes, there is usually a sudden liquidation that exaggerates the price movements.

Lastly, the participants are advised to be sensitive to significant exchange or regulatory news because these may lead to sentiment changes without involving macro or flow effects.

To summarize, ETF flows, Fed policy, on-chain exchange activity, derivatives positioning, and regulatory developments are included in the watchlist. These indicators are the guide on the way to navigate the crossroads of crypto, and they are hints of whether the market will go up further, flatten, or stagnate.

Limitations and Closing Nuance

Any recap of a short-horizon market, e.g., the Sept 13-16, 2025, window, should be viewed with reservations. To begin with, the data sources have latency and methodological differences. Daily net flow reports of ETFs (The Block, Farside, BitBo, etc.) can contain slightly different reported values of their daily net flows depending on timing conventions, custodian reporting windows, or creations-redemptions. On-chain data has analogous constraints: wallet grouping, labelling exchanges, and API latency imply that the numbers can be regarded as directional but not accurate. To make trading or asset-allocation choices, the participants are encouraged to cross-reference various datasets and use primary disclosed data whenever feasible.

Second, ETH year-end base case projections by analysts like Citi are scenario models, not projections. There exist varied predictions on the assumptions of adoption, stakeholder returns, growth of fee markets, and regulatory acceptance. An extreme dependence on one institutional note can make it difficult to focus on the allocation of results. The change in ETH targets, which starts with conservative to extremely bullish, is indicative of the contingency of future research.

Third, the market is still macro-sensitive. The close relationship between the expectations on the U.S. Federal Reserve policy and the flows of cryptos implies that sentiment can change rapidly with new CPI prints, employment announcements, or Fed instructions. It takes only a single hawkish comment to uncoil ETF-based inflows and re-establish technical structures in a matter of days. This vulnerability serves as a reminder that the liquidity dynamics across the globe are highly conditioned to establish short-term crypto resilience.

Finally, the structural shift of crypto, which is the change in the exchange flow dominated by retailers to institutional flows issued by ETFs, is not a complete change yet, either. Although this transfer seems to be conducive to liquidity and legitimacy, the transfer of ownership to passive vehicles and the possibility of long-run volatility behaviour also cast doubt. To comprehend this change, it is necessary not only to follow the prices daily but also to place crypto within the financial framework.

Conclusion

The week between Sept 13-16, 2025, highlighted two forces that are defining crypto market trends today: institutional ETF flows and macro policy expectations. The two of them create the hinge around which the near-term price action revolves.

The inflows into Bitcoin and Ether funds in ETFs are no longer an isolated phenomenon; they are the structural re-orientation of demand. With more institutions favouring regulated, product-friendly custodians, ETFs are a sure means of inflow that can stabilize trade ranges, enhance liquidity, and make crypto a legitimate part of larger portfolios. The recent consolidation of Bitcoin around the still figure of about 115,000 dollars and the mid-range of Ether around the 4k mark point to the fact that the price levels are maintained not only through the efforts of speculative interest, but also through gradual commitments of managed money. This is an indication of a more long-lasting support base than previous cycles.

Meanwhile, it is the macro that is the final judge. The anticipated 25 bps reduction by the Federal Reserve is priced as a bullish motivation, although flows are sensitive to Fed communications; any variation in this narration would promptly alter the sentiment. In this respect, crypto is tied to the liquidity situation in the world, despite the shift in the number of investors.

To the participants, the forward look will be divided into three distinct watch points:

ETF flow momentum: Does daily inflow continue, decelerate, or turn around?

Fed transparency: Does the Fed cut rates as anticipated, or are they postponed based on data?

On-chain/derivatives stress events On-chain/derivatives stress events On-chain/derivatives stress events Will structural risks (liquidations, exploits, exchange shocks) interrupt institutional flows?

The conclusion is not easy to draw, although volatility will persist in the short term, the medium-term trend will depend upon whether ETFs cement themselves as a channel of dominant demand within a conducive macro environment. In case it continues, crypto will have the ingredients of a new institutional-led cycle. In case one of them collapses, the market will have to re-price swiftly.